Living cost support in 2018-19: how do different parts of the UK compare?

An announcement is expected soon on living cost support for students in Scotland, expanding on a few things made public this weekend. This looks likely to be the formal response to last year’s Scottish Government review of student funding.

This post provides some context for any announcement, by bringing together information for the four UK nations on living cost support for full-time undergraduate students in higher education. Unlike the Diamond review in Wales in 2016, the Scottish review did not make proposals for post-graduate or part-time students, although it did also cover support in FE.

Why make comparisons? Mainly because claims of being “best in the UK” have been used repeatedly to justify developments in Scotland over recent years, and might be expected to be made again. The main message from the material below is that comparisons here are complicated: beware of sweeping claims to “bestness”.

Total value of maintenance support

The analysis below covers support for students studying HE-level courses, whether at college or university.

(i) Away from home

The majority of students from all UK nations live away from the parental home, including those from Scotland. These students will tend to face the highest costs, especially for housing.

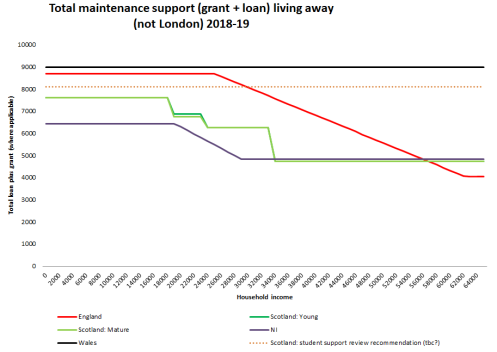

The graph below shows the total value of support, i.e. any grant plus loan, currently on offer for students living away from home in 2018-19 in the different UK nations. Also included (dotted line) is the proposal from the Scottish student support review. The graph shows what students get if they take out their whole loan: different approaches in the UK to loan and grant are looked at in more detail below.

Scotland on current plans sits some way below Wales and England, except at the highest incomes, with a maximum of £7,625. It is above Northern Ireland at incomes below £34,000, and marginally below at higher ones. Generally, families in Scotland are expected to find a lot more upfront help than those in Wales or England, especially once income tips £19,000 and until it reaches over £50,000. The Scottish system is often held up as being distinctive in the UK because it is not based on “ability to pay” (the FM repeated this at the weekend): but if your pre-tax household income is £25,000, your family is currently expected to find some £2,500, or more, a year upfront towards your keep than they would be in some other parts of the UK.

If the Scottish government accepts the review’s recommendation that all students should have access to £8,100, by increasing student loans, and implements it in time for 2018-19, total support will still be higher in Wales, but only in England at incomes up to £29,000. The change would substantially improve the total support offered at lowish-to-middle incomes..

In the nations other than Scotland students get around an additional £2,000 if they study in London and are living away from home (not shown in graph for simplicity), meaning that for students in London, Scotland is the least generous nation.

(ii) Living at home

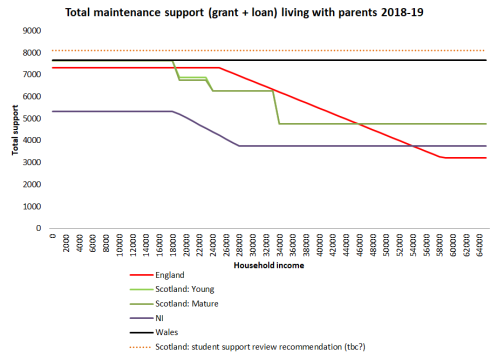

Scotland has a larger minority of students living in the parental home than elsewhere (it is hard to get good data, but the figure looks to be around 45%). In the other UK nations, such students get around £1,500 less than those away from home, but the Scottish system does not make this deduction, so Scotland compares better for this group, sitting just £25 below Wales at incomes below £19,000. It is also above England up to £19,000, but is substantially less generous for some incomes not much above that. It is always better than Northern Ireland.

If the student support review recommendation is accepted, then Scotland will have the highest support in the UK for those living at home. Having the highest combined grant and loan package for this group can only offer a limited basis for claiming “bestness” however, as:

- Much of this support is offered as loan, while these students appear less likely than others to borrow, and may even live at home partly to reduce their borrowing, meaning the notional amount is less likely to be realised in practice. Students living at home who choose only to take their grant will do better in Wales and Northern Ireland (see below).

- Many students do not have the option of living at home.

- It is students who live away from home who face the highest costs.

(iii) Part-time undergraduates

Part-time students in Wales and England will receive a pro rata share of the main living cost package from 2018-19. On current arrangements, this will not be the case in Scotland and the student support review did not include part-time students its costings. So the Scottish government would have to go further than the review recommendations to do anything for this group.

(iv) FE students

Scotland is already providing much more support to this group than other UK nations (I don’t have charts for that: it is evident from a general scan of the situation). Adopting the review proposal to put them onto the total value of support as HE students would reinforce that. However, the review recommends doing this through both an increase in bursary and the introduction of loans into FE. Take up of loans is already lower among HE students in college than in university: it seems likely therefore that take-up among FE students in practice of the new full £8,100 grant and loan package would be limited. The review’s proposed higher maximum grant of £4,050 would however still compare well with other parts of the UK, just by itself.

Overall comparison

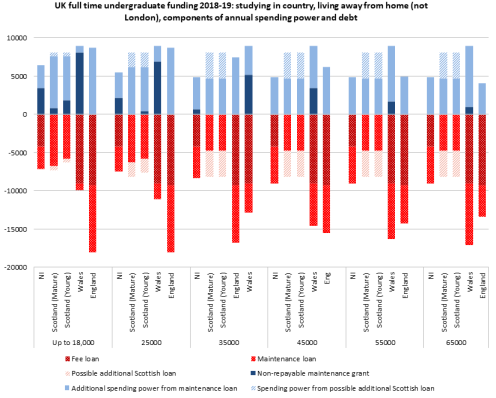

A full comparison of living cost support means looking at the balance of grant and loan, and once loan comes into play, it is misleading not to bring in debt for fees.

The chart below shows how systems compare at various incomes for those living away, but studying in their home nation. For the English and Welsh, crossing a border within the UK makes no substantial difference, but for the Scots and Northern Irish, you have to imagine a £9,250 additional fee charge if they wish or need to do so.

Above the line in blue is the value of upfront living cost support (“spending power”), separated into grant and loan, with the impact of acting on the review recommendation shown as an additional element for Scotland. Below the line in red is the associated debt, separated for fee and living cost loans. The living cost debt mirrors the spending power given by the loan.

(The chart for those living at home would be similar, but takes about £1,500 off the maintenance loan elements above and below the line for the nations other than Scotland.)

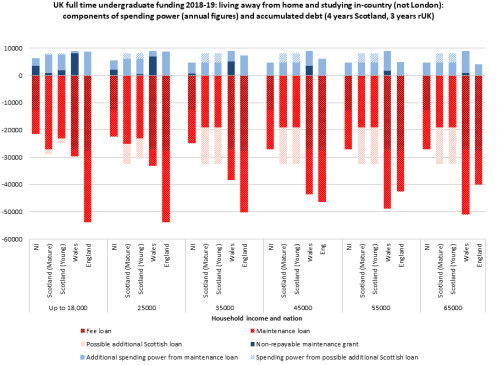

The comparison above works best for those on identical length courses, such as one and two year HNs, or degrees which take the same length of time in all parts of the UK. However, an honours degree in Scotland takes 4 years compared to a more typical 3 in the rest of the UK. The chart below is therefore a better comparison for most honours degree students. Above the line it still shows the annual value of living cost support, as this is consumed immediately; but below the line, it now shows accumulated debt over the period of study.

If an extra year of study is factored in, Scotland is already similar to Wales, especially for mature students. At low incomes, these two will be near-identical, in terms of total annual living cost help and accumulated debt, if the Scottish review recommendations are accepted. For mature students at the lowest incomes (which is most mature students), the marginally higher debt in Wales is all due to their great spending power. [Note added: The difference in interest rates while students study is not added in here. Relative to lower interest Scotland/NI, that adds £3-4k for those at incomes up to £35k in Wales, but more for those where gap is already larger, ie with higher borrowing in Wales and England.]

At lower incomes, if you can save a year of study by not being in the Scottish system, Northern Ireland is already the lowest debt nation, reflecting that living cost loans are very limited, as well as fees being lower than in Wales or England. It will be the lowest debt nation on this model at all incomes, if the Scottish review recommendations are implemented, again reflecting its less generous living cost support.

England is always much higher, and Wales joins it as income rises, yet again because it uses loan to offer more living cost support at higher incomes. This chart cannot show:

- how far take-up of loan will vary in practice, especially of living cost loan. Maintenance loan take-up is 85%+ in the rest of the UK, but only about 70% in Scotland, where there is substantial non-borrowing especially among students from higher incomes. How far higher income Welsh students use their new, higher loan will be something to watch.

- the effect of the higher interest used in England and in Wales. In Wales this is partially off-set by a flat-rate write-off of £1,500 as soon as a graduate starts to repay, which will remove some or all of the the effect of higher interest during study, but not later.

- how far headline debt will translate into actual repayments: higher debts are less likely to be repaid in full than lower ones.

The last point is critical, but very hard to predict. Higher interest will further increase the total cost of repayments, in England and in Wales. But write-offs are expected to have most impact on the highest borrowers. Then again, even among the English and Welsh, some people will still feel the full force of their initial borrowing: there will be higher earners who receive no write off, and middle earners who do benefit from a write-off, but mainly or all of accumulated interest.Thus the difference in costs by country actually experienced over time should be less stark on average than shown in the graph, especially for women, who tend to earn less than men, but the variation round the average for students who left HE with similar debt will be very large for England especially.

Is anyone best in the UK?

It really does depends who you are, what you care about, who you regard as equivalent to who, and how you take into account that some of the difference in debt is because students get different levels of benefit in different systems.

Scotland is already best for FE-level students, regardless of any further announcements made this week.

For HE, if your family finds it hard or impossible to support you, Wales’ post-Diamond review package works best, taking the pressure off family contributions across the board. At lower incomes it offers this help almost all in the form – grant – likeliest to be taken up, so that overall debt for this group is similar to that for fee-free Scots, especially mature Scots.

If you are going to be a pretty lower earner who is unlikely to pay back much of your debt (a group which will disproportionately be women), again the Welsh system looks best: generous upfront support at little later cost. However, if the Scottish review is implemented, future low earners who can live with their parents while they study will get most to live on in Scotland.

Similarly, if you are part-time, and cannot contemplate studying without help with living costs, you want to be in Wales or otherwise England, where there’s at least the option of a loan. In both those nations, however, you will need to be willing also to borrow for fees.

On the other hand, if you are full-time, young and from a family who can manage to cover much of your living costs in cash and kind, and want to and can get a place in Scotland, Scotland offers the best deal, with the option even of emerging debt-free. Don’t be a Scot who wants to study in London, though: they get an unusually raw deal of relatively poor living cost help plus fees. The Scottish system is generally poor for border crossers, as is the Northern Irish one: both are high debt, for limited upfront help.

Both England and Scotland suffer from skewing debt towards those at lower incomes, which is an ethical rather than a practical point, complicated by the theoretical possibility that later write-off will mostly smooth out differences in initial borrowing: that is much more likely to hold true in England, but even then only up to a point, and doesn’t look at first sight to hold well for Scotland at all, but ask me again about that when I have finished the PhD.

In other words, the only way to deal with any claims about bestness in student support is to test them in detail. The question is always, best in what way, for who? Best of all of course might be for governments (and others: the recent student support review didn’t cover itself with glory here either) to stop making general claims like this at all. With a much-trailed announcement coming soon in Scotland, I wouldn’t however advise throwing away your bingo card just yet.

Comments are closed.