Student support review #6: filling a gap in the review report and the case for accepting its recommendation in HE

As this post noted, surprisingly the recent report of the Scottish student finance review did not set out what its proposals would mean at different incomes. Nor did it show how entitlements would change at different incomes under its recommendation. This post aims to fill that gap, providing a few charts which are missing from the review report. It argues that although the change is limited, and restricted to increasing loan, there is a case for these changes in HE, especially from the perspective of those at middle incomes. It also looks at how, on paper at least, the proposal addresses Scotland’s current regressive distribution of student debt: it argues however that more use of grant would do that better (using the Welsh approach to funding a flat-rate system as an example).

The arguments about loans in FE are not discussed here: they raise different issues.

How entitlements change

The review’s formal recommendation (the”hybrid option”) is considered here, not the “aspirational” higher grant one. Under the hybrid option, the review recommends no change to HE grants.

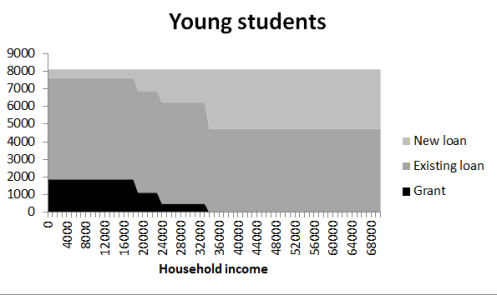

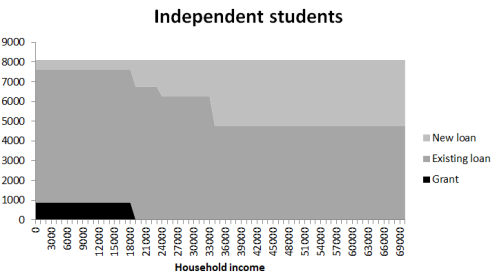

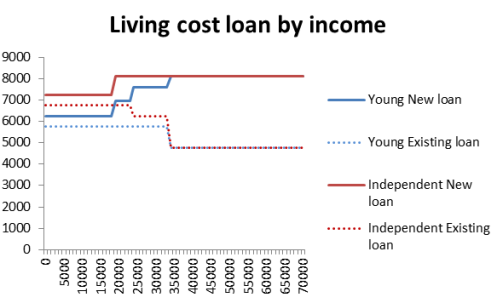

The two graphs below, one for young students and one for independent students who are (and are assumed to remain) on a lower grant rate, show how the recommendation would change loan entitlements in HE at different incomes.

The proposals for HE have a quite limited impact at the lowest incomes. Mature students tend to fall heavily into the lowest income group, so the changes for them in practice would be particularly limited.

The changes would be more substantial however for those at incomes of £19,000 and over, and especially at £34,000 and up. This would reduce the pressure on these families to contribute upfront, provided students are willing to borrow more. The amount currently available, especially for those at just over £34,000, implies a pretty large contribution relative to household income (and the current Scottish system expects substantially more from families at this level than is common in the UK more generally). This is the real “ability to pay” issue.

In the absence of any other funding there is a case for just releasing this extra loan, especially from the perspective of those at middle incomes: it wouldn’t justify any grandiose claims, but the best shouldn’t be the enemy of the better-than-now and (unlike when grants were cut in 2013) this wouldn’t make lower income students have to borrow more just to stand still, and it ought to go a little way to spreading debt more evenly by income (see below). It would though sit uncomfortably with the Scottish Government’s long-standing, if increasingly detached from reality, anti-debt rhetoric.

The aspirational higher grant HE option and FE recommendation can’t be modelled, because no information is provided on how the review’s costings assume grant would reduce as income rises, in either case.

Debt distribution

The new model is more progressive on paper, with expected loan now increasing, rather than falling, as income rises. How far the additional loan is taken up at high incomes (and if so, not used as a cheap form of saving for the future) would determine how far changing the model on paper alters the distribution of debt students incur while studying in practice. I think take-up at higher incomes, especially for essential living costs, will be patchy. But it would still be more than now.

I worry also about nest-egg building by those from high incomes, as a new form of hidden advantage, because of the low interest rate on student loans here. We could apply higher interest to loans to those from better-off households (but we won’t). Even without that, however, I think on balance this risk is worth taking for a few years, but ideally the use of the new loans at higher incomes would be monitored.

As noted elsewhere, the change would be achieved by increasing debt at middle and higher incomes rather than bringing it down at lower ones. Using grant to reduce debt at lower incomes would be a more certain way of achieving a less regressive loan distribution.

What happens with higher grant

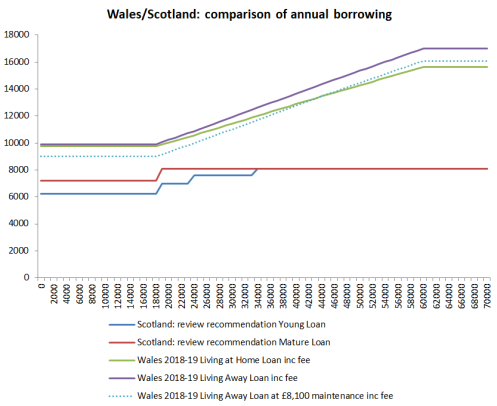

The Welsh plans for 2018-19 show how the same starting point – a flat-rate support entitlement – can produce a very different assumed levels of debt and debt distribution with more use of maintenance grant.

(Figures for Wales taken from the table on this site, with estimates by this author for the income points not shown.)

The graphs above of course exclude additional borrowing for fees, which adds an additional flat-rate amount at all incomes. But even after that a strong skew will remain. A footnote considers separately how total actual borrowing would compare between the two systems (not that much at low incomes), but that’s a different point, which also reflects different decisions about how much of the cash budget to commit to HE, as well as the split of investment in grants and fees.

The Scottish government could achieve the same targeted effect as above, at no extra cost and retaining its lower average debt levels than Wales. That would mean investing more cash in grants and less in fees. The review was prevented from exploring such options.

One further, important advantage of a high grant approach to providing a flat-rate entitlement is that take up of living cost support is likely to be much higher at low incomes. Even where people are willing to take on fee debt as an unavoidable price of getting into higher education, it’s plausible they will be less willing to take on living cost debt and, say, work excessive hours or limit their choices to what they can do living at home. Already in Scotland, among young students qualifying for means-tested grant, between a fifth and a quarter don’t use their living cost loan. The review disappointingly does not acknowledge, far less explore, this.

Conclusion

I don’t understand why the review doesn’t include the income charts at the top of this post. Equivalent ones are prominent in the Diamond review, from which the review has borrowed its central concept of a flat-rate entitlement, and the required figures must have been available to the review, for them to produce the published costings. They usefully bring out that in HE it’s those at middle to lowish incomes for whom the decision whether or not to accept the recommendation is likely to matter most. They get a pretty raw deal at the moment with living cost help.

It’s clearer however why the government might prefer these charts not to be in. They illustrate how much the Scottish system depends on loans to underwrite living costs, and how much the review’s strict remit forces it further down that road. The charts above throw into sharp relief that the rhetorical association so often made by Scottish ministers between fees and debt is far from the whole story.

All figures used above are here Student support review_changes by income

Footnote

Two things affect the comparability of total borrowing between the new Welsh and recommended Scottish system:

- the addition of fee debt in Wales, at £9,000 for those in country, and

- different values of total spending for those living at home (£7,650) or away (£9,000), compared to the single Scottish amount of £8,100.

However, the difference in total annual borrowing at the lowest incomes, especially for mature students, will not be very large. It is close enough that a low-income Welsh mature student who decided to limit themselves to the same £8,100 total as in Scotland would have marginally less final debt after three years (3 x £9,000 = £27,000) than a similar Scot after four years (4 x £7,225 = £28,900).

The figures above are for those studying in their home nation. To adjust for border crossing from Wales, add £250. Border crossers from Scotland will have £9,250 more debt.

Comments are closed.